TheJakartaPost

Please Update your browser

Your browser is out of date, and may not be compatible with our website. A list of the most popular web browsers can be found below.

Just click on the icons to get to the download page.

Popular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPopular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsWhy market share of Islamic banks is so small in Indonesia

According to the Global Advisors’ Islamic Finance Outlook Report for 2016, no Indonesian Islamic banks were ranked in the top five largest banks based on assets in Southeast Asia. This is an alarming situation for the industry and regulators. Thus, it evokes a question: Is the market becoming saturated for Islamic finance? The public believe that Islamic banks are still unable to tap into its market potential. The basis for such an argument is simple as indicated by the large size of the Muslim population and the size of the Muslim middle-class.

Change text size

Gift Premium Articles

to Anyone

Share the best of The Jakarta Post with friends, family, or colleagues. As a subscriber, you can gift 3 to 5 articles each month that anyone can read—no subscription needed!

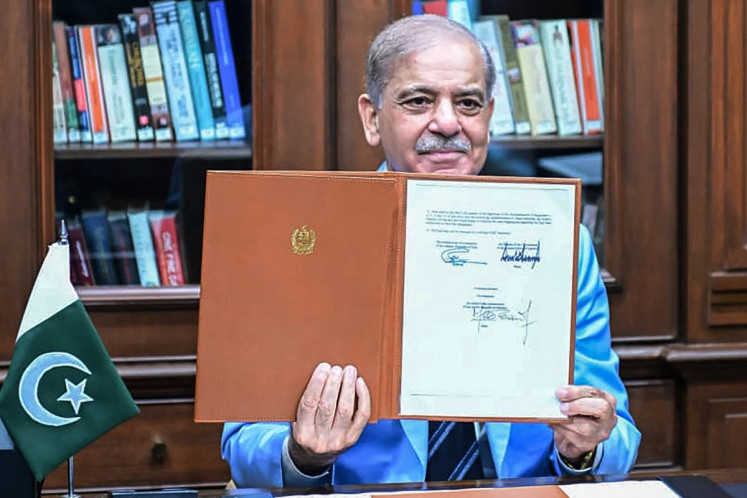

A BCA Syariah staff member serves a customer after an opening ceremony at its headquarters on Jl. Jatinegara Timur in East Jakarta on April 5, 2010. (The Jakarta Post/P.J. Leo)

A BCA Syariah staff member serves a customer after an opening ceremony at its headquarters on Jl. Jatinegara Timur in East Jakarta on April 5, 2010. (The Jakarta Post/P.J. Leo)

T

he performance of the Islamic banking industry in Indonesia has yet to satisfy the public’s expectations. Although with a market of more than 200 million Muslims, Islamic banks in Indonesia still face difficulties luring more customers and increasing their assets. For three consecutive years, the market share of the sharia banks in the country stood still at less than 5 percent.

According to the Global Advisors’ Islamic Finance Outlook Report for 2016, no Indonesian Islamic banks were ranked in the top five largest banks based on assets in Southeast Asia. This is an alarming situation for the industry and regulators. Thus, it evokes a question: Is the market becoming saturated for Islamic finance?

The public believe that Islamic banks are still unable to tap into its market potential. The basis for such an argument is simple as indicated by the large size of the Muslim population and the size of the Muslim middle-class.

Indeed, if one calculated roughly, around 40 percent of 200 million Muslim are at the productive age of between 20 and 40 years old, not counting the affluent segments aged between 40 and 60 years old. Unfortunately, being a Muslim does not necessarily mean that he or she has good literacy on Islamic finance.

The failure to seize Muslim customers is the latent problem of Islamic banking in Indonesia. There are at least four reasons contributing to this situation.

First, there have not been enough endeavors to adequately explain what Islamic finance is all about. This problem occurs because of a scarcity of good talent. Bankers at Islamic banks are mostly the same talents from the counterparts.

Therefore there is a tendency to explain Islamic financial products and services in “conventional language”. Explaining Islamic financial products could be cumbersome to someone who does not have adequate knowledge of fiqh muamalat.

Second, customers often perceive Islamic banks’ services as “poor” and “expensive”. Islamic bank customers often complain about the long and complicated bureaucratic transaction processes, the lack of IT services and the expense.

Such a perception arises because, unlike borrowing and lending activities of conventional banking, Islamic products are mostly based on trading contracts, in which the bank sells and the customer buys. This sell-buy activity evokes costs, such as taxes and other legal fees that consequently add up the transaction costs.

The third, Islamic finance has yet to operate on a level playing field with the conventional banks in terms of regulations and the tax system.

Besides lack of regulatory support, the industry does not have fresh ideas from academics on innovation. While Malaysia took an early initiative to set up institutions dedicated to nurturing talent and advancing Islamic finance as a serious field of knowledge, Indonesia is a follower.

Only recently, have universities and higher learning institutions begun seriously advancing the field and offering Islamic finance programs to young people.

There are four strategies to cope with such problems.

First, misconceptions about Islamic finance must be adequately explained. Regulators and authorities could employ social resources, such as communal meetings, to assume a bigger role in educating the market.

Second, in order to promote the role of Islamic banks, the institutions are required to be on the same level playing field with their counterparts. Regulatory products, taxes and legal systems must be customized according to the characteristics of the industry so it could grow.

Third, when Islamic banks are the prima facie institutions of the Islamic financial system, a professional service is important. Islamic banks must be serious in advancing the entity as the forefront of ethical-professional service providing. At this junction, training staff and front-liners to demonstrate an attitude that satisfies customers’ expectations is really an investment.

Fourth, Islamic banks should get away from the “conventional mindset” and look through the basic principles of Islamic finance to come out with innovative products and services. At this junction, the institutions could work closely with universities, financial experts and Muslim scholars to design products that not only comply with the ruling, but are also cheap and accessible to anyone.

Islamic finance is more than just Islamic banks. The system offers a complete organization of financial services; from banking to capital market, from project financing to micro-finance, and from design of macroeconomic policy to wealth-management. Despite its adherence to Islamic financial law, the system works on the basis of a universal value: risk-sharing. The system supports sharing economic risks as the most efficient method for risk management and thus the more profitable one.

By risk-sharing, monetary resources would flow to the highest valued use. At this juncture, the system re-couples financial markets with real sectors.

A brighter outlook is predicted. Indonesian Islamic banks are gaining momentum as shown by high asset growth in the regions as their services expand. Therefore, on whether the market for Islamic finance has been saturated, the answer is absolutely not.

Moreover since government, bankers, academics and policymakers are now on the same page about advancing the industry and exploring the system, we could only hope to see Islamic financial institutions gaining more share of the market in the near future to bring benefit to our economy.

***

The author is a doctoral candidate in the Islamic finance program at the International Center for Education in Islamic Finance (INCEIF) in Kuala Lumpur, Malaysia.

---------------

We are looking for information, opinions, and in-depth analysis from experts or scholars in a variety of fields. We choose articles based on facts or opinions about general news, as well as quality analysis and commentary about Indonesia or international events. Send your piece to community@jakpost.com.