TheJakartaPost

Please Update your browser

Your browser is out of date, and may not be compatible with our website. A list of the most popular web browsers can be found below.

Just click on the icons to get to the download page.

Popular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPopular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPolicy mix to outwork coronavirus outbreak

The national policy mix is a necessary and proper approach to outwork the potentially exponential growth of COVID-19 cases.

Change text size

Gift Premium Articles

to Anyone

Share the best of The Jakarta Post with friends, family, or colleagues. As a subscriber, you can gift 3 to 5 articles each month that anyone can read—no subscription needed!

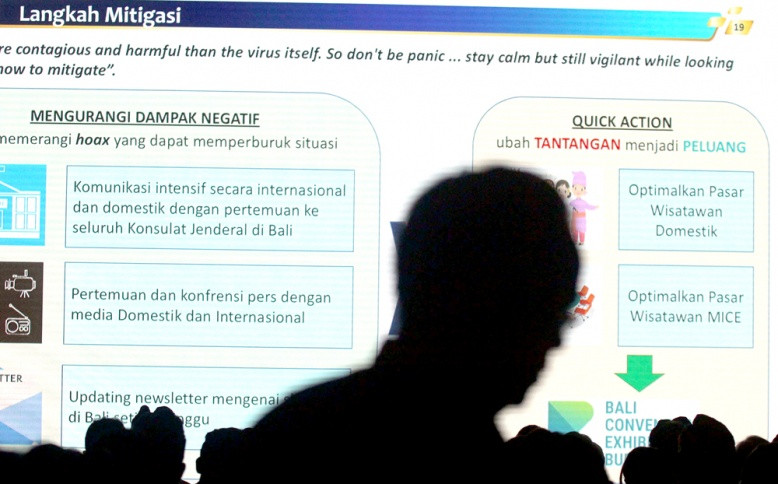

Contagious: The Bali representative office of Bank Indonesia uses a screen to explain measures the government has been taking to address the COVID-19 outbreak and its impacts on industry during the launch of the Bali Convention Exhibition Bureau on Feb. 13. (JP/Zul Trio Anggono)

Contagious: The Bali representative office of Bank Indonesia uses a screen to explain measures the government has been taking to address the COVID-19 outbreak and its impacts on industry during the launch of the Bali Convention Exhibition Bureau on Feb. 13. (JP/Zul Trio Anggono)

T

he yet undiscovered cure for COVID-19 has intensified knock-on effects for global economies. The disruption of productivity continues due to quarantines or lockdowns as a major measure to fight the virus. No matter how the prior fundamental domestic economy worked, all economies of the “infected states” have suffered from this pandemic.

Unlike the disease, curing a macroeconomic downturn has its formulas through monetary policy, fiscal policy and a banking safety net. Bank Indonesia (BI) as Indonesia’s monetary authority continues to introduce preemptive measures to preserve credit expectations as it is fully committed to maintaining liquidity tension in the market. It executed a triple intervention policy and promoted domestic non-deliverable forwards to modulate the volatility of the exchange rate. BI also adjusted the seven-day reverse repo rate to a lower level of 4.5 percent and relaxed the reserve requirement to bolster credit growth.

On the fiscal front, the pandemic forces countries toward deeper fiscal deficits due to revenue shortfalls. The Indonesian government has announced several packages of fiscal stimulus for health care, a social safety net for “blue-collar” and informal workers, and incentives for affected businesses and industries. The Finance Ministry also estimated the fiscal deficit was up to as high as 5 percent of gross domestic product. Those measures, however, are essential for combating COVID-19 and its economic consequences. Fiscal stimulus is hugely important to ensure a stronger long-term economy.

President Joko “Jokowi” Widodo has signed a regulation in lieu of law (Perppu) stipulating emergency policies and measures to prevent the escalating tension in the country’s economic and financial sector. The Perppu gives sets of comprehensive “cures” in anticipating economic turbulence and aims to avoid further financial downside risks in the course of the pandemic. It does so by mandating some substantive roles to relevant authorities, which enables them to work together more closely through the existing Financial System Stability Committee (KSSK).

In an escalated situation, extraordinary adjustments are necessary. Most macroeconomists must have agreed with this stepped-up effort. In the language of Paul A. McCulley, the former chief economist of Pacific Investment Management Co. (PIMCO), “the ‘bank of dad’ needs to remain open!” This implies that, in the occurrence of shocks, any alternative source should be considered. Jokowi’s Perppu not only provides broader leeway for the fiscal stimulus but it also effectively strengthens authorities’ roles while working toward efficiencies in the banking prudential supervisory and deposit insurance scheme. The paradigm now slightly shifts toward a “nationwide macroeconomic policy mix”. The focus is nothing more than to prevent economic calamity.

Article 16 (1) of the Perppu renders statutory delegation for BI more accessible for economic and financial stability. Article 16 (1) c shapes a “joint venture” between fiscal and monetary policy by authorizing the central bank to function as the “dealer of last resort”. BI will serve as a backstop to the government when the market is not efficiently functioning. It allows fiscal robustness to combat the virus and mitigate profound economic damage. This, of course, is a temporary measure that must be executed prudently and promptly adjusted when the balance is struck.

The price tag on inflation as being contemplated in Article 19 (3) b should be carefully considered; yet the “policy mix” is also essential to maintain nominal aggregate demand and thus pump-priming the economic growth in unusual and exigent circumstances.

The downfall of economic absorptive capacity must also be anticipated from this public health crisis. In such an occurrence, the stimulus would fulfill the gap, thereby supporting effective countercyclical response of monetary policy. Soon after the private sector can generate spending normally, the government could unwind the stimulus.

Governments across the world are now facing more stringent funding in the fight against COVID-19. However, the situation is still different from the global financial crisis in 2008, which emerged because there were excessive private debts to fund speculative assets. Today, we face a distinct problem arising from, it seems, a divine act striking hundreds of countries. The last resort lending through the “forwardlooking” approach for systemic banks according to Article 16 (1) b of the Perppu hence should also be deemed necessary as an additional contingency measure to avoid the pandemic infecting the financial system. In addition, measures on strengthening deposit insurance resources in the Perppu also provide hope for banks to continue serving the economy.

In addition to the containment of COVID-19, macroeconomic stability should be the primary urgency. It should make sectoral interests convergent. The monetary sector requires a well-executed fiscal policy as well as financial stability to retain each of their powers to achieve institutional goals. The important point now is to maintain effective coordination across authorities and to dynamically adjust the measure toward any turn of events.

The national policy mix is a necessary and proper approach to outwork the potentially exponential growth of COVID-19 cases. Economic leaders have given examples of “holding hands” by solidly pursuing the collective goal to avoid and solve macroeconomic problems. If anything, this step should be applauded as a progressive movement. It is now their responsibility to prudently implement the “policy mix” in good faith and to squeeze any moral hazards to zero.

Against all odds, there are now more reasons to be confident economically and, in the end, it depends on the level of our forbearance to boost common rationality to win this war.

***

Bank Indonesia legal affairs department staff member. The views expressed are his own.