TheJakartaPost

Please Update your browser

Your browser is out of date, and may not be compatible with our website. A list of the most popular web browsers can be found below.

Just click on the icons to get to the download page.

Popular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPopular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsFocused on Java, P2P lending not as ‘inclusive’ as hoped

A study from professional services firm EY suggests that changes in tax policy and higher loan limits may help Indonesia improve financial inclusion.

Change text size

Gift Premium Articles

to Anyone

Share the best of The Jakarta Post with friends, family, or colleagues. As a subscriber, you can gift 3 to 5 articles each month that anyone can read—no subscription needed!

I

mproved financial inclusion has been one of the promises of the peer-to-peer (P2P) lending business from the get-go and is reflected in a mandate for P2P firms under Financial Services Authority (OJK) Regulation No. 77/2016.

However, players in the industry are falling short of that promise, as most of their loans go to borrowers on Java Island, including micro, small and medium enterprises (MSMEs), and relatively few go to less developed regions of the country.

Analysts say a closer partnership between P2P lenders and the government to facilitate loan disbursement outside of Java, as well as changes in tax policy and larger maximum loans could facilitate financial inclusion.

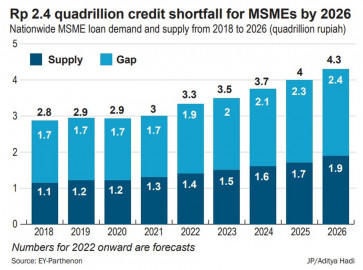

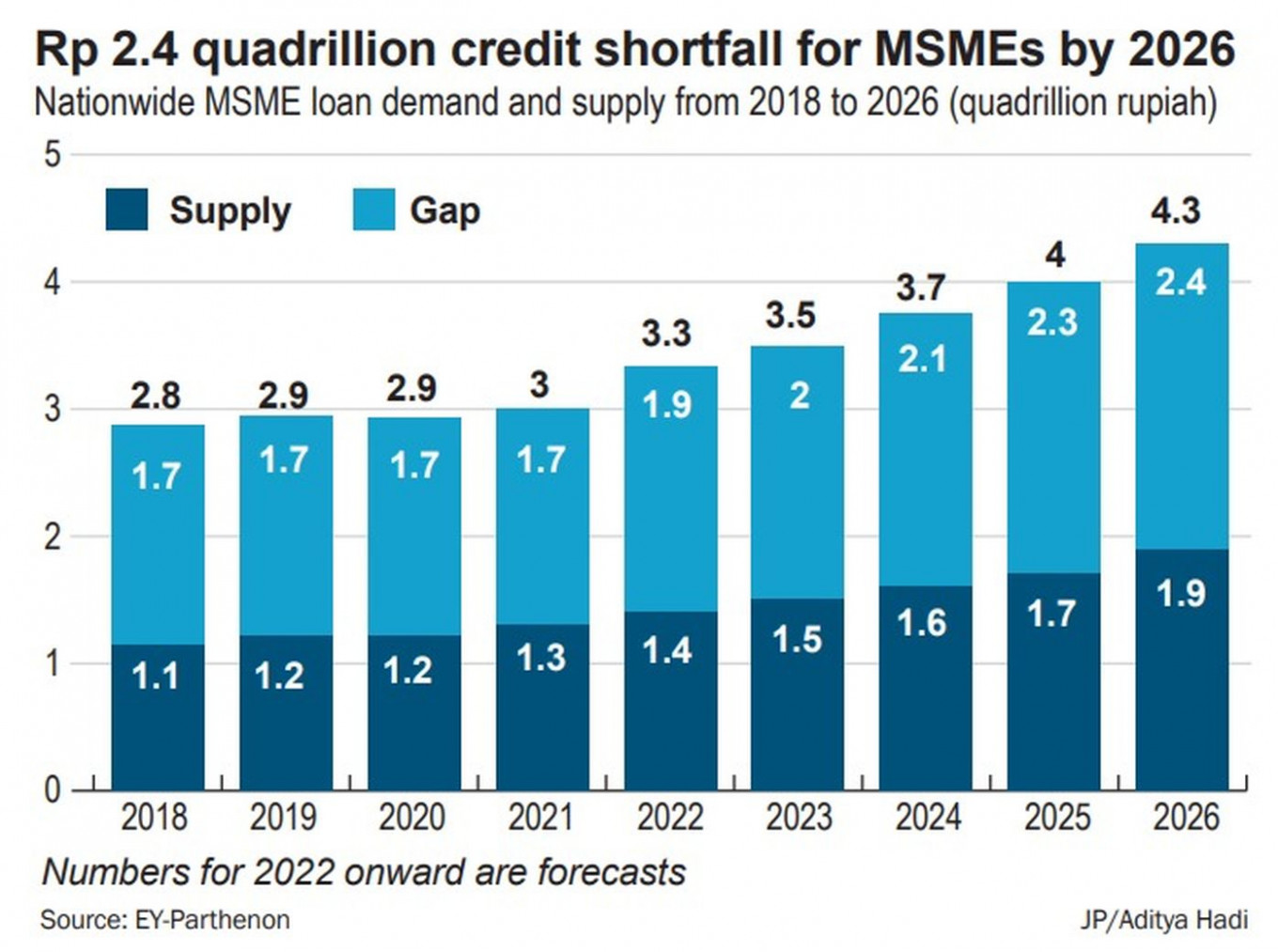

A recent study by Ernst & Young (EY) Indonesia's consultancy arm, EY-Parthenon, predicts that loan demand from MSMEs in the country will rise to Rp 4.3 quadrillion by 2026, which may result in a loan gap of Rp 2.4 quadrillion.

According to the study, which was conducted with support from the Indonesian Fintech Lenders Association (AFPI), 60.5 percent of the demand for MSMEs financing in 2026 would come from Java Island, where the majority of businesses are located.

The study forecasts that the role of state-owned banks in lending to MSMEs will continue to increase in the coming years, as they have been mandated to disburse at least 30 percent of their loans to that segment. On the other hand, the contribution of private banks, regional banks and multifinance firms is expected to either stagnate or drop.

Anugrah Pratama, a partner at EY Parthenon Indonesia, said P2P lenders could play a bigger role with the surge in MSME loan demand, as their risk appetite and platform accessibility were more suitable to the sector.