TheJakartaPost

Please Update your browser

Your browser is out of date, and may not be compatible with our website. A list of the most popular web browsers can be found below.

Just click on the icons to get to the download page.

Popular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPopular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsDemutualization, state and market: Who guides the guide?

Healthy markets rely on a paradox. They are built by the state but function best when the state does not dominate their day-to-day outcomes.

Change text size

Gift Premium Articles

to Anyone

Share the best of The Jakarta Post with friends, family, or colleagues. As a subscriber, you can gift 3 to 5 articles each month that anyone can read—no subscription needed!

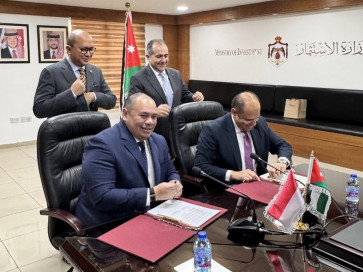

Danantara chief investment officer Pandu Sjahrir (bottom left) and Jordan Investment Fund director Zaher Al Qatarnaeh (bottom right) sign a memorandum of understanding on Dec. 9, 2025, to explore joint investments in strategic sectors in Jordan. The signing was also witnessed by Danantara CEO Rosan Roeslani (top left), who also serves as Investment and Downstream Minister, alongside Jordanian Investment Minister Tareq Abu Ghazaleh. (Courtesy of/Danantara)

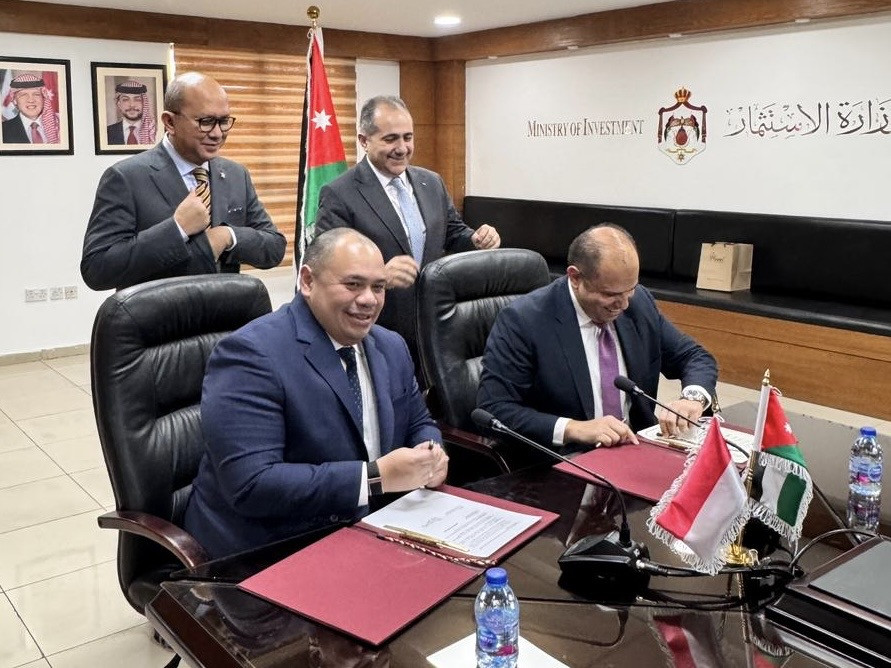

Danantara chief investment officer Pandu Sjahrir (bottom left) and Jordan Investment Fund director Zaher Al Qatarnaeh (bottom right) sign a memorandum of understanding on Dec. 9, 2025, to explore joint investments in strategic sectors in Jordan. The signing was also witnessed by Danantara CEO Rosan Roeslani (top left), who also serves as Investment and Downstream Minister, alongside Jordanian Investment Minister Tareq Abu Ghazaleh. (Courtesy of/Danantara)

A

s Indonesia prepares to demutualize the Indonesia Stock Exchange (IDX), state asset fund Danantara is weighing whether to take a significant stake. This move is described as a long overdue reform that will strengthen governance, improve transparency and expand domestic financing.

All of that may be true. But ownership of a stock exchange is not just a corporate matter. It quietly shapes who gets access to capital and who does not. The real question is not simply who will own the IDX, but how that ownership may influence the flow of money across the economy.

In emerging markets, exchanges rarely function as neutral marketplaces. They mobilize household savings, support large domestic firms and often serve as shock absorbers during financial stress. Governments therefore see them as tools for channeling investment into areas the private sector tends to avoid, such as infrastructure or heavy industry with long payback periods.

From this perspective, linking the exchange to a state asset fund is not ideological. It is a practical response to a familiar problem.

Left alone, markets sometimes underinvest in projects that are economically important but commercially unattractive in the short run. Government Regulation No. 10/2025 gives Danantara an unusually central role. It consolidates state ownership of major enterprises under a single institution reporting directly to the president.

Unlike many sovereign wealth funds that invest abroad, Danantara is meant to operate mainly at home, managing productive assets inside the national economy. In effect, the state becomes not only the referee of the market but also one of its largest players.

Owning part of the exchange would not allow officials to dictate trades or pick winning stocks. Influence works in subtler ways. Exchanges set listing rules, disclosure standards, index membership and the mechanics of raising capital. These decisions sound technical, but they determine which companies can tap deep pools of funding and which remain on the margins. Control over the marketplace does not decide outcomes directly. It shapes the field on which outcomes become possible.