TheJakartaPost

Please Update your browser

Your browser is out of date, and may not be compatible with our website. A list of the most popular web browsers can be found below.

Just click on the icons to get to the download page.

Popular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPopular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsGoing beyond pension to strengthen the social security system

The country's social security system, now over 20 years old, might need reforms for an across-the-board upgrade to reflect contemporary conditions and trends, such as an aging population and a shift from traditional, family-based elderly care, as well as inclusion of a growing informal sector.

Change text size

Gift Premium Articles

to Anyone

Share the best of The Jakarta Post with friends, family, or colleagues. As a subscriber, you can gift 3 to 5 articles each month that anyone can read—no subscription needed!

Dozens of workers rally on Feb. 18, 2022, outside the Manpower Ministry on Jl. Gatot Subroto in South Jakarta to demand it cancel a ministerial regulation stipulating a minimum age of 56 for people to start withdrawing from their pension funds. (Antara/Aditya Pradana Putra)

Dozens of workers rally on Feb. 18, 2022, outside the Manpower Ministry on Jl. Gatot Subroto in South Jakarta to demand it cancel a ministerial regulation stipulating a minimum age of 56 for people to start withdrawing from their pension funds. (Antara/Aditya Pradana Putra)

O

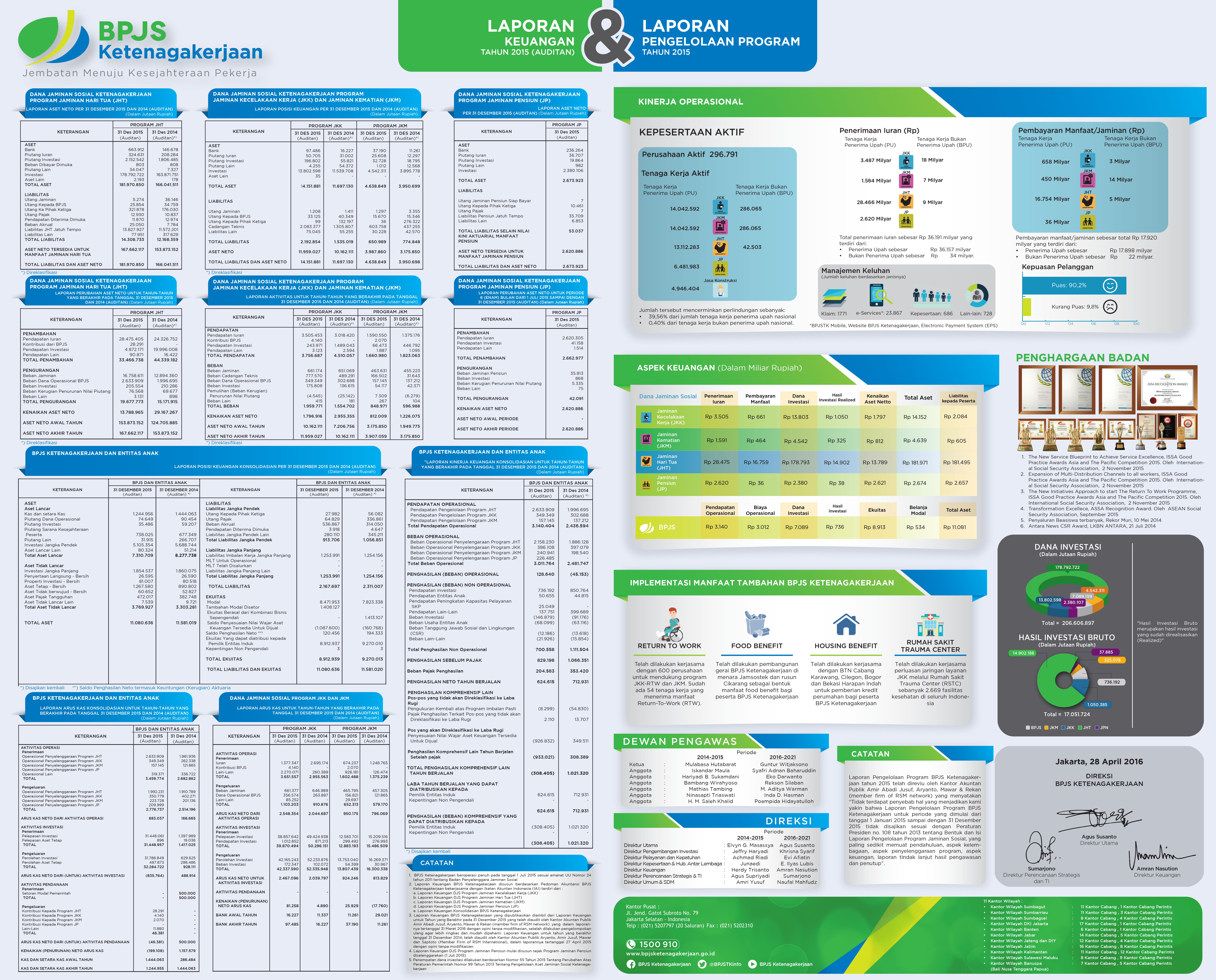

ver the past decade, the National Social Security System (SJSN) has made significant strides in expanding coverage in Indonesia. Initially focused on civil servants, military, police and formal private workers, it is now underway to cover a broader population.

Participation in workers social security surged from 19.2 million in 2015 to 41.5 million in 2023, and now encompasses over 30 percent of the workforce. Meanwhile, the sharp rise in managed assets (BPJS Ketenagakerjaan) from Rp 178 trillion (US$11.1 billion) in 2015 to Rp 712.3 trillion in 2023 not just shows its financial strength, but also allows the introduction of unemployment benefits (JKP) that has bolstered resilience, particularly during the global shocks of COVID-19.

Just two years after the pandemic’s peak, Indonesia experienced a significant recovery – the poverty rate dropped back to single digits and open unemployment returned to below 5 percent – highlighting the effectiveness of social security in mitigating the crisis.

At least three major challenges currently affect the future role of the SJSN.

First are demographic and structural challenges. Since 2021, the country has officially entered the aging population phase, with one in every 10 Indonesians now elderly (Statistics Indonesia/BPS, 2023). This demographic shift increases the demand for reliable and sustainable social protection mechanisms.

However, the SJSN struggles with low active participation rates, especially among informal workers, who make up around 60 percent of the workforce. Public literacy about the system remains limited which further hinders enrolment, creating a disconnect between demographic needs and the system’s effectiveness, posing a serious challenge to its long-term sustainability.

Second is ineffectiveness of the old-age security (JHT) program, which is currently misaligned with its original purpose. It functions more as a short-term savings scheme rather than a true retirement protection tool. Participants are allowed to withdraw benefits for non-retirement reasons, and contribution enforcement is weak (DJSN, 2022). This undermines its role as a safety net for old age, weakening financial preparedness for retirement.

{kind=link}