TheJakartaPost

Please Update your browser

Your browser is out of date, and may not be compatible with our website. A list of the most popular web browsers can be found below.

Just click on the icons to get to the download page.

Popular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsPopular Reads

Top Results

No results found. Please check your search term and try again

Can't find what you're looking for?

View all search resultsFintech case exposes troubling misapplication of competition law

Recent crackdown on fintech lending ignores a critical reality: these "price-fixing" measures were actually regulatory mandates designed to protect consumers. By applying a rigid competition framework to a co-regulated market, the KPPU risks stifling financial inclusion and deterring the very investors the nation needs.

Change text size

Gift Premium Articles

to Anyone

Share the best of The Jakarta Post with friends, family, or colleagues. As a subscriber, you can gift 3 to 5 articles each month that anyone can read—no subscription needed!

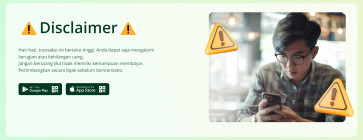

A warning displayed on a peer-to-peer lending website on Sept. 13, 2024, part of efforts by the Financial Services Authority (OJK) and financial industry to discourage people without the ability to repay from applying for loans. (JP/Aditya Hadi)

A warning displayed on a peer-to-peer lending website on Sept. 13, 2024, part of efforts by the Financial Services Authority (OJK) and financial industry to discourage people without the ability to repay from applying for loans. (JP/Aditya Hadi)

I

ndonesia’s largest digital finance competition case has reached a decisive conclusion, marking a watershed moment for the nation’s regulatory landscape. Following proceedings that began on Aug. 14, 2025, the Business Competition Supervisory Commission (KPPU) delivered its decision on March 26, 2026, ruling that 97 financial technology (fintech) peer-to-peer (P2P) lending platforms, all members of the Indonesian Fintech Lenders Association (AFPI), violated Article 5 of Law No. 5/1999 on Monopolistic Practices and Unfair Business Competition.

The case centers on an interest rate ceiling set collectively within AFPI’s code of conduct, initially 0.8 percent per day, later reduced to 0.4 percent. The anti-monopoly body stated the platforms breached Article 5, which prohibits agreements among competitors to fix prices in the same relevant market. Consequently, the KPPU imposed substantial fines, ranging from Rp 1 billion (US$59,000) to over Rp 100 billion, sending shockwaves through the digital economy.

Price-fixing is one of the most serious offenses in competition law. In many jurisdictions, it is treated as per se illegal because it replaces independent decision-making with collective control, theoretically harming the consumer by default. However, the fintech P2P lending context in Indonesia complicates this traditional doctrinal approach. By applying a rigid per se framework, the KPPU may have overlooked the broader "rule of reason," which allows for an analysis of whether a practice actually results in a net procompetition or public benefit.

While trade associations have long been viewed with caution, often seen as potential vehicles for coordination, this case does not arise from purely private, "smoke-filled room" coordination among competitors. AFPI operates under a formal co-regulatory framework supervised by the Financial Services Authority (OJK). The interest rate ceiling was not a predatory move to gouge consumers; rather, it was adopted in accordance with written directions from the OJK. These directions were issued amid mounting public concerns over predatory "loan shark" behavior, opaque fee structures and the potential for systemic consumer harm. In this context, the cap was a regulatory compliance measure intended to stabilize a nascent industry, not a mechanism to suppress competition.

The economic structure of fintech P2P lending further challenges a simplistic price-fixing narrative. Unlike traditional brick-and-mortar markets where firms might compete on a single, uniform price, these platforms rely on highly individualized, risk-based pricing driven by proprietary credit-scoring algorithms.

A shared maximum ceiling does not automatically produce identical pricing outcomes. If platforms retain autonomy over their datasets, machine learning models and underwriting parameters, substantial price differentiation continues to occur below the cap. In such an environment, competition naturally shifts from "headline rates" to the sophistication of predictive analytics, the efficiency of risk management, and the quality of the user experience. To view a maximum safety cap as a "fixed price" is to misunderstand the digital mechanics of modern lending.

More fundamentally, the KPPU’s decision turns on the definition of the "relevant market." The assumption that all 97 fintech platforms operate within a single, homogenous market deserves careful scrutiny. From a consumer perspective, Sharia-based profit-sharing platforms are not fully substitutable with conventional interest-based lenders. Similarly, a high-frequency, short-term consumer loan does not directly compete with medium-term productive financing aimed at micro, small, and medium enterprises (MSMEs).